This report was written by Alexandra Albers-Schoenberg, Research Associate at the INSEAD Global Private Equity Initiative (GPEI), with input from Ian Potter, Distinguished Fellow at GPEI, and under the guidance of Claudia Zeisberger, Professor of Entrepreneurship and Family Enterprise at INSEAD.

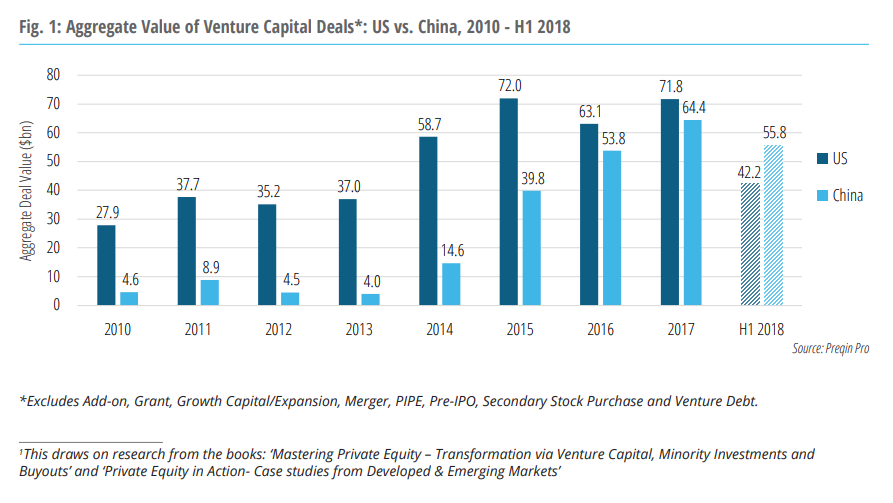

China’s venture capital (VC) sector has moved into the fast lane. For the first time, Chinese start-ups have attracted more funding than their US counterparts. In the first half of 2018, an astonishing $56bn was invested in China-based early-stage companies, leaving the US in second place with $42bn, a third less (Fig. 1). The huge investment flowing into China was driven by multibillion-dollar funding rounds for Ant Financial, Mobike, Manbang Group, Pinduoduo, and Ping An Healthcare. Ant Financial raised the largest single fundraising round in history with Series C funding of $14bn.

China venture watchers have had little time to relax in the past eight years. In 2017, an aggregate $64bn was deployed in early-stage companies in China, 14x more than in 2010 (when the aggregate investment was a mere $4.6bn). With such momentum, no wonder the media is suggesting that China is on its way to becoming the world’s largest VC market. But can the growth rate be sustained? What challenges lie ahead – and what will it take for China to move into pole position in the race for global venture capital?

To answer these questions, our study evaluated the four pillars of a thriving VC ecosystem: 1) the supply of ideas and entrepreneurs, 2) the presence of reliable stewards of capital, 3) the availability of adequately priced risk capital, and 4) the ability to recycle capital and return it to investors. For each pillar, we identified recent achievements and remaining gaps in the Chinese VC market.

1) SUPPLY OF IDEAS AND ENTREPRENEURS

While the reputation of Chinese VC was, at times, something of a “copycat” culture – imitating products and services from the West – companies in China are now developing disruptive technologies that are proprietary, and the shift is underscored by a herd of newly established “red unicorns”.

Unicorns – privately held, venture-backed companies with a valuation in excess of a billion dollars – first emerged in the US, but Chinese names have proudly joined the global unicorn rankings, reflecting an increase in private capital and positive investor sentiment regarding VC opportunities in China. Preqin data shows that, of all unicorns3, 31% are from China (98 out of 321). While the US has created the most unicorns to date (162 out of 321), China is catching up fast.

Interestingly, China is the birthplace of some of the largest unicorns: five of the top 10 current mega-unicorns5 originate from China, with the remaining five from the US (Fig. 2). Ant Financial, the payments and financial services arm of Alipay, which is currently valued at $150bn, holds the number one position, followed by Uber, the US car-hire service, at $71.5bn. The third is Uber’s main competitor Didi Chuxing, the Chinese ride-hailing, artificial intelligence, and autonomous technology company, which in 2016 acquired Uber’s China unit (Uber retains a 17.7% stake in Didi Chuxing).

China is the birthplace of some of the largest unicorns: five of the top 10 current mega unicorns originate from China.

China is the birthplace of some of the largest unicorns: five of the top 10 current mega unicorns originate from China.

China is the birthplace of some of the largest unicorns: five of the top 10 current mega unicorns originate from China.

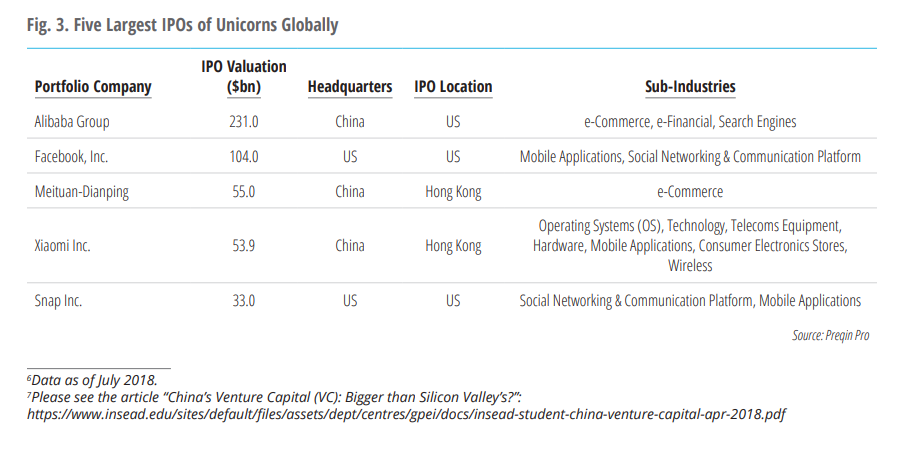

China is the birthplace of some of the largest unicorns: five of the top 10 current mega unicorns originate from China.Additionally, three of the top five IPOs of unicorns (in terms of company valuation at IPO) were Chinese companies (Fig. 3). Number one is Alibaba Group, with a valuation of $231bn at IPO and raising $25bn, making it the largest-ever IPO for any company in history, followed by Facebook with a valuation of $104bn and raising $16bn. The third is MeituanDianping, which just recently listed its company with a valuation of $55bn at IPO, where it raised $4.2bn.

The success of the red unicorns has spurred a culture of entrepreneurship in China, inspiring millions of young Chinese to follow suit, encouraged by government efforts to support innovation and entrepreneurship.

The backbone of China’s high-tech industries comprises the so-called ‘high technology zones’ that have developed throughout the country. As of 2017, China has 146 high technology zones, including the renowned Zhongguancun Science Park, often referred to as the “Silicon Valley of China”. Located close to some of the country’s most prestigious technology universities and research institutes, the government supports these zones by offering benefits and incentives, helping to create business hubs.

Nonetheless, for China’s VC ecosystem to mature further, a few key concerns need to be addressed. For example, China has difficulty conquering the global labor market compared to the US. Whereas Silicon Valley attracts top talent from around the world, China is not quite on the list of preferred startup locations. Stumbling blocks include the language barrier and cultural differences. Additionally, despite new policies having been implemented to protect patents and endorse intellectual property rights, China is still criticized for – and some may argue being held back by – a lack of strong intellectual property and trademark laws.

All in all, there is an ample supply of ideas and entrepreneurs in China and the move towards innovation has been spectacular. Yet China still faces a few hurdles on its way to becoming a true innovation nation.

2) PRESENCE OF RELIABLE STEWARDS OF CAPITAL

Opportunities in China’s growing tech sector have prompted many domestic and foreign VC firms to enter the market. While domestic firms have close connections to government bodies, universities and local enterprises, there is a shortage of experienced local venture capitalists with track records. Foreign firms often have more experience in VC management, but face investment restrictions and lack local connections.

Of the 465 investors globally that invested in the 98 Chinese unicorns that form Preqin’s dataset, it is remarkable that 66% have a local presence in Mainland China and a further 9% in Hong Kong. Only 13% of investors are investing directly from the US, and barely any are located in Europe.8

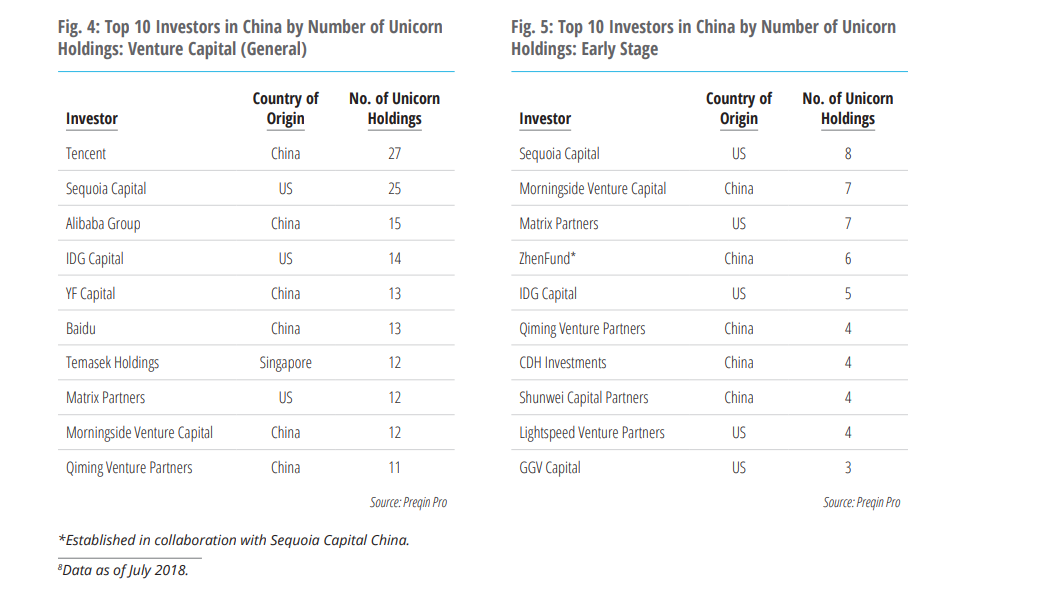

To establish which investors have been the most successful, we ranked them according to the number of red unicorn holdings. The three Chinese tech giants – Baidu, Alibaba, and Tencent (or the ‘BAT trio’) – are all in the top five. Tencent, the leading provider of internet value-added services and one of the largest corporate venture investors worldwide, tops the table with the most red unicorn holdings: it has equity stakes in 27 of the 98 Chinese unicorns (Fig. 4). Alibaba Group and Baidu have invested in 15 and 13 unicorns respectively. The BAT trio not only invests in early-stage companies but also provides an attractive exit channel by acquiring many of the companies in the long run. In the US, some of the big corporates have also invested in multiple unicorns, but they are fewer in number and invest less consistently than their BAT counterparts.

Excluding the BAT trio, the investor with the most red unicorn holdings in China is US VC firm Sequoia Capital with 25. This is followed by IDG Capital, which was one of the first firms to bring VC into China, with 14 red unicorn holdings.

As the above ranking does not take into account the timing at which the investors entered nor the magnitude of the value invested, it cannot be inferred that investors with the most unicorn holdings achieve the best fund performance. Typically, those that invest in the early-stage funding rounds (seed, angel or Series A) make higher returns on investment at exit than those that invest in the later rounds.

When we rank the top early-stage investors by a number of unicorn holdings, Sequoia Capital leads the table, having invested in the early rounds of eight unicorns (Fig. 5). Second is Morningside Venture Capital with seven, followed by Matrix Partners and ZhenFund with six each. It is interesting to note that while the BAT trio is not present among the top 10 early-stage investors, a noticeable number of foreign VC firms hold the leading positions.

In short, there is an increasing number of local and foreign investors in the Chinese VC market, and our analysis finds that the BAT trio plays a key role. Additionally, some of the backers of early-stage unicorns are from the US or local ‘spin-offs’ of US venture capital firms, which may imply a shortage of local VC fund managers in early-stage VC investments.

3) AVAILABILITY OF ADEQUATELY PRICED RISK CAPITAL

The large influx of capital into early-stage funds and direct deals in China comes from various sources. We have categorized the domestic Chinese VC investors into institutional investors (including corporate investors), high-net-worth individuals (HNWIs)and government vehicles. There are also foreign investors investing in Chinese VC, typically through foreign VC funds. Restrictions and even prohibitions of foreign investment in certain industries, especially the financial and internet services sectors, although gradually loosening do at this stage still hinder international capital from entering the market.

Institutional investors contribute significantly to the Chinese VC market and, in particular, strategic investors, which are the most prominent institutional investors in China. As already mentioned, the BATtrio has investments in many early-stage companies. Other prominent Chinese institutional investors, which either invest in early-stage funds or do direct VC deals, are financial investors ranging from investment companies and asset managers to insurance companies and wealth managers.

HNWIs and families are also a key source of VC funding in China. The number of HNWIs in China has grown significantly over the past 10 years. Whereas older wealthy individuals – the first generation to benefit from China’s open-door policy – prefer to manage their assets themselves, younger HNWIs are more willing to seek professional advice, and hence invest in professionally managed vehicles such as VC funds. The predominance of local HNWIs in the Chinese VC market can be explained by the rising size of their assets, a lack of attractive alternative investment opportunities in China, as well as restrictions on investing capital abroad.

Additionally, the government provides VC capital to early-stage companies through government-backed programs – including the so-called government guidance funds (GGFs). These usually take the form of a fund of funds investing in private or public-private funds. Their main goal is to boost certain strategic industries such as big data, artificial intelligence or robotics. GGFs have been around for over 10 years; by the end of 2016, there were more than 1,000 GGFs with an estimated combined size of RMB 5.3tn ($798bn). The majority of GGFs’ capital comes from tax revenue or state-backed loans.

Foreign investors are also significant participants in the Chinese VC market. However, not only are their restrictions for foreign investment, especially in the key technology sectors but getting money out of the country once invested also remains a challenge for them. Therefore, while direct investments by foreign investors are quite limited, many foreign investors participate in the Chinese VC market through vehicles such as offshore VC funds. In fact, a significant portion of the LP base of the top VC funds listed in Fig. 4 and Fig. 5 consists of foreign investors.

In conclusion, there is a vast source of capital flowing into China‘s venture capital market. Seeking to benefit from VC opportunities in China, both institutional and HNW investors are pouring money into the industry. Additionally, the government is building a framework and funneling capital to support the VC system as well as to spur innovation and entrepreneurship. Foreign investors also participate in the Chinese VC market; however, their participation still seems largely restricted to investments through offshore funds.

4) ABILITY TO RECYCLE CAPITAL AND RETURN IT TO INVESTORS

Exits are an essential part of the venture capital investment cycle and ultimately determine whether a deal is successful or not. It is yet to be seen whether the capital flowing into Chinese start-ups yields attractive returns. There are some concerns from investors that the VC market in China is experiencing a ‘bubble’ and that Chinese companies are currently overvalued. In recent times, there has been a series of shortfalls in actual IPO valuations as compared to target valuations. Xiaomi, for example, went public at a valuation significantly lower than originally anticipated.

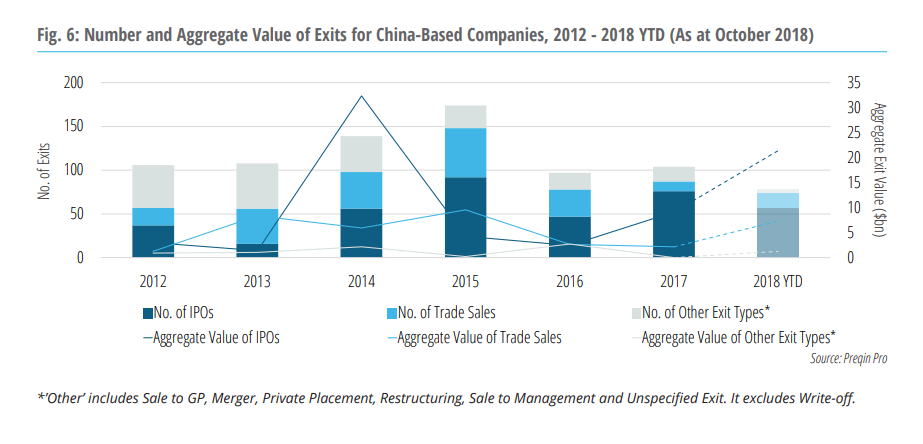

According to Preqin data, the most frequent exit channel for Chinese portfolio companies is the IPO. As of Q3 2018, 57 Chinese companies have undergone an IPO with an aggregate exit value of $21bn globally, 2.3x the amount exited in 2017. Some of the well-known IPOs include Xiaomi, iQiyi, Pinduoduo as well as NIO. However, none of these examples were listed in Mainland China – iQiyi, Pinduoduo, and NIO were all listed in the US, and Xiaomi in Hong Kong.

One reason for companies to list overseas is that their brands become better known internationally, helping the business to expand and attract a global investor base. Another is that listing a company in China has its complexities. Many early-stage companies have had difficulty listing on local stock markets (mainboards in Shanghai and Shenzhen, SME board in Shenzhen) due to strict listing requirements regarding profitability and capital thresholds, a lengthy listing process (more than two years on average), as well as a ban on variable interest entities (VIE) in the domestic equity market.

In 2009, ChiNext was launched on the Shenzhen Stock Exchange to attract early-stage companies offering less stringent requirements than the main boards and the SME board. In 2012, the NEEQ (National Equities Exchange and Quotations) – also called the New Third Board – was established to provide an alternative exit route for Chinese SMEs that cannot list on other exchanges. The NEEQ is an over-the-counter securities trading market that does not require prior business performance or a financial vetting process. However, many in the industry are not optimistic about the future of NEEQ due to its relatively low liquidity.

Recognizing that the stock market environment in mainland China is suboptimal – and in order to attract companies to list in China and stimulate the Chinese capital market – the government has recently put in place new policies to fast-track new listings of certain companies. Furthermore, the China Securities Regulatory Commission (CSRC) gives preferential treatment to VC funds to dispose of their equity, allowing them to exit their investments earlier post-IPO. The government has also announced the launch of China Depositary Receipts (CDRs), a form of shares that will allow China-based investors to gain exposure to foreign-listed Chinese companies. However, so far no CDRs have been issued. Xiaomi, which listed its shares in Hong Kong in July 2018, was supposed to offer the first CDRs but has put off the mainland share offering for now, implying another failure for the stock market ecosystem.

The second most common exit route for Chinese portfolio companies is the trade sale. As of Q3 2018, 17 Chinese companies have exited through trade sale with an aggregate exit value of $7.3bn, 3.3x the amount exited in 2017 (Fig. 6). The BAT companies are big buyers of venture-backed companies and have so far acquired the lion’s share. The trio often starts with relatively small stakes in early-stage companies but then in some cases takes over the entire company. The largest trade sale of a Chinese portfolio company was that of Youku Tudou Inc., the Chinese video-streaming giant, to Alibaba in 2015. This year, the two largest transactions were the sales of Ofo Bicycle to Alibaba and Mobike Ltd. to MeituanDianping. However, since trade sales require a high level of professional assistance, one of the biggest difficulties is a shortage of experienced M&A intermediaries given the short history of M&A in China. Moreover, many Chinese entrepreneurs seem unwilling to fully exit their companies, preferring the IPO route.

All in all, the most common exit routes are IPOs and trade sales. Despite continuous efforts to improve its IPO rules, China has not yet managed to find an optimal solution. Trade sales are another popular exit strategy and the biggest acquirers in the market are the BAT companies. It remains to be seen whether the exit options are mature enough to absorb the many exits to come.

IN CONCLUSION

Looking at the growth of the Chinese VC market over the past several years, it looks promising that China could become the market-leader of VC in the world. Data suggest that both the money flowing into early-stage companies as well as the money flowing back to investors is currently on the rise, indicating the development of a full investment cycle empirically. However, the VC market in China is still very young, and it is too early to conclude whether its current growth is sustainable or not. China is also well known to forge its own path, making it difficult to compare to the historical development of Western markets.